United States

United States

Rate cuts are on the agenda and yields are near post-pandemic highs. A golden age for bond markets is potentially getting started. Now could be the time to take advantage.

You’re invited

The first rate cutting cycle in 15 years (apart from during the pandemic) potentially beckons.

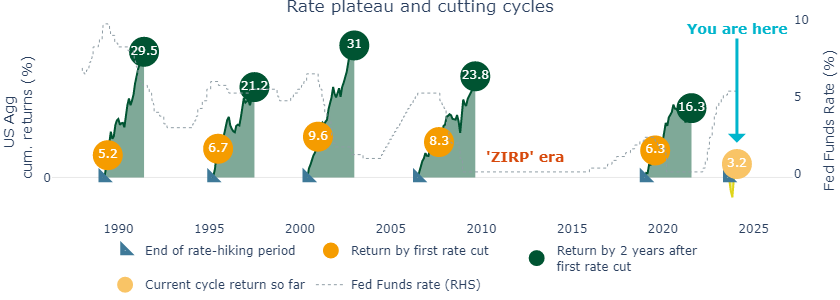

The last five cycles were golden ages for bond markets, with the US Agg returning between 16% and 31% (Figure 1) and US credit1 between 21% and 32%2 in the two years following the last rate hike. Those cycles particularly benefited those that invested early, locking in fixed rate coupons at the top of the rate cycle and achieving price appreciation as rates fell.

Figure 1: The latest bond market golden age could be just beginning

Source: Bloomberg, Insight. Bloomberg US Aggregate Bond index. February 2024. Please see index descriptions at the back of the document.

So far this cycle, the US Agg has only returned 3% and US credit less than 5%. This implies that the latest golden age is potentially just beginning. There could be more to come over the next few years if the Fed executes a steady stream of rate cuts from the second half of 2024 in line with its own projections3.

Bonds can potentially deliver a higher degree of certainty to your portfolio

Higher yields mean fixed income investors are entering a market with a stronger tailwind.

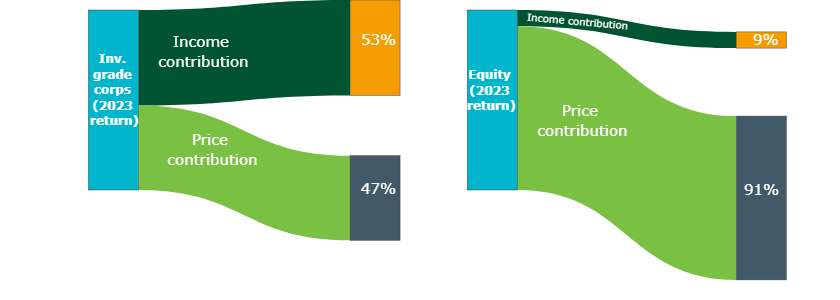

Yield is the primary driver of returns for long-term investors. Since 2000, 102% of US investment grade total returns are attributable to yield4. For large-cap equities, over the same period, only 45% of returns are attributable to dividends4.

Even for short-term investors, bond yields will potentially help stabilize annual returns. In 2023, an unusual year in which bond prices were particularly volatile, coupon income still drove most returns, at 53%, whereas equity investors saw only 9% of their return from dividend income (Figure 2).

Figure 2: Even in a volatile 2023, income has been the driver of fixed income returns

Source: Bloomberg, Insight calculations, January 2024. Past performance is not indicative of future results. Investment in any strategy involves a risk of loss which may partly be due to exchange rate fluctuations.

Yields remain near post-pandemic highs

Unlike cash investors, bond investors can lock in today’s yields for years to come. Those in cash may consider now to be an ideal time to move further out the curve; Fed rate cuts will lower cash yields without providing any accompanying diversification benefit.

Additionally, bonds may benefit investors looking to diversify their equity portfolios or crystallize their equity gains. Historically, low bond yields meant an expensive opportunity cost from switching any exposure into bonds. However, fixed income yields are now closer to long term equity returns (Figure 3), meaning investors may give up much less in future potential equity gains by allocating to fixed income.

Figure 3: Yields are still close to their post-pandemic highs

Source: Bloomberg, Insight, January 2024. MBS = Bloomberg US Mortgage Backed Securities (MBS) Index, Investment grade = Bloomberg US corporate bond index, ABS = Bloomberg US Agg ABS Index, Emerging market hard currency = Bloomberg Emerging Markets Hard Currency Aggregate Index, High yield = Bloomberg US Corporate High Yield Bond Index, S&P 500 = S&P 500 Total Return Index. Please see index descriptions at the back of the document. Past performance is not indicative of future results. Investment in any strategy involves a risk of loss which may partly be due to exchange rate fluctuations.

Additionally, moderating economic growth may be a headwind for equity markets.

Time to consider dollar-cost averaging as well as opportunities to “buy the dips”

We believe investors should consider the opportunity to reallocate some of their cash and equity exposure to fixed income now, deploying dollar-cost-averaging.

Market volatility is also worth keeping an eye on as expectations have shifted over the last few months. Volatility may continue, which means active investors may find abundant opportunities to find more compelling entry points.

Either way, we believe investors should look to complete their desired reallocations into bonds before the timing of the first rate cut becomes crystal clear.

Consider a global approach to seek to capture the golden age’s full potential

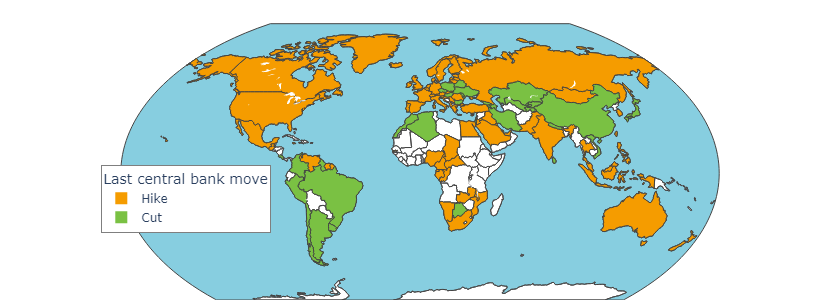

Although we may have to wait a bit longer for rate cuts in the US than the market hopes, rate cuts have already started elsewhere (Figure 4):

Figure 4: The global rate cutting cycle has kicked off

Source: Macrobond, National Sources, Insight Investment, February 2024.

The US was the worst performer out of the largest 20 countries in the Global Agg index in 2023. Whereas the US Agg returned 5.5%, the Global Agg (US dollar hedged) returned 7.2%5.

As with most years, we believe that a globally diversified approach would have added value. As such, a diligent and fully global fixed income approach may be the optimal way to benefit from the global cutting cycle.

We think a fixed income golden age has started. Try not to miss it.

Most read

Fixed income

August 2022

Is it time to consider high yield?

Liability-driven investment, Fixed income

July 2022

Liability Driven Insights: A pit stop on your de-risking journey

Fixed income

April 2023

Catch a rising star: fallen angels may hold the key

Global macro

April 2022