United Kingdom

United Kingdom

In markets like high yield, passive solutions are hampered by costs and difficulties accessing bonds and traditional active strategies are typically concentrated and volatile. You either must accept ‘index minus’ outcomes or manager selection risks.

We think there is a better way: a systematic investment approach seeking advantages of both passive and fundamental active strategies, while controlling their shortcomings.

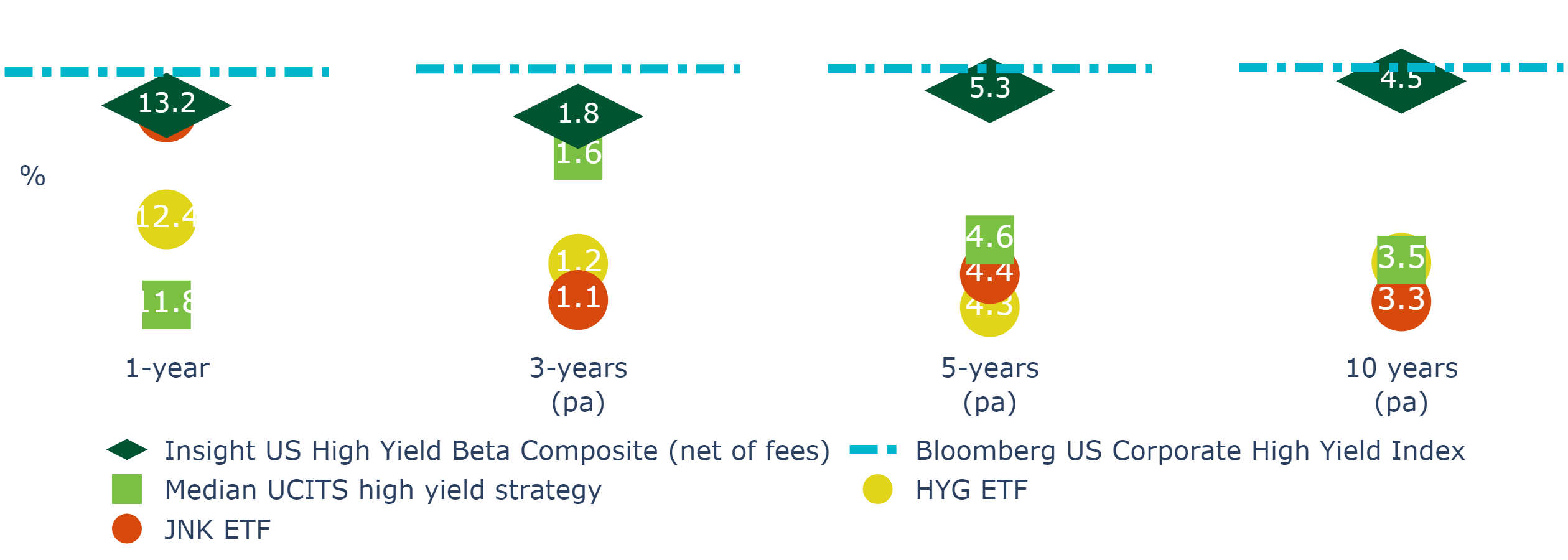

Figure 1: A systematic approach may be the best way to achieve high yield returns with low tracking error1

Passive US high yield strategies deliver “index-minus” results

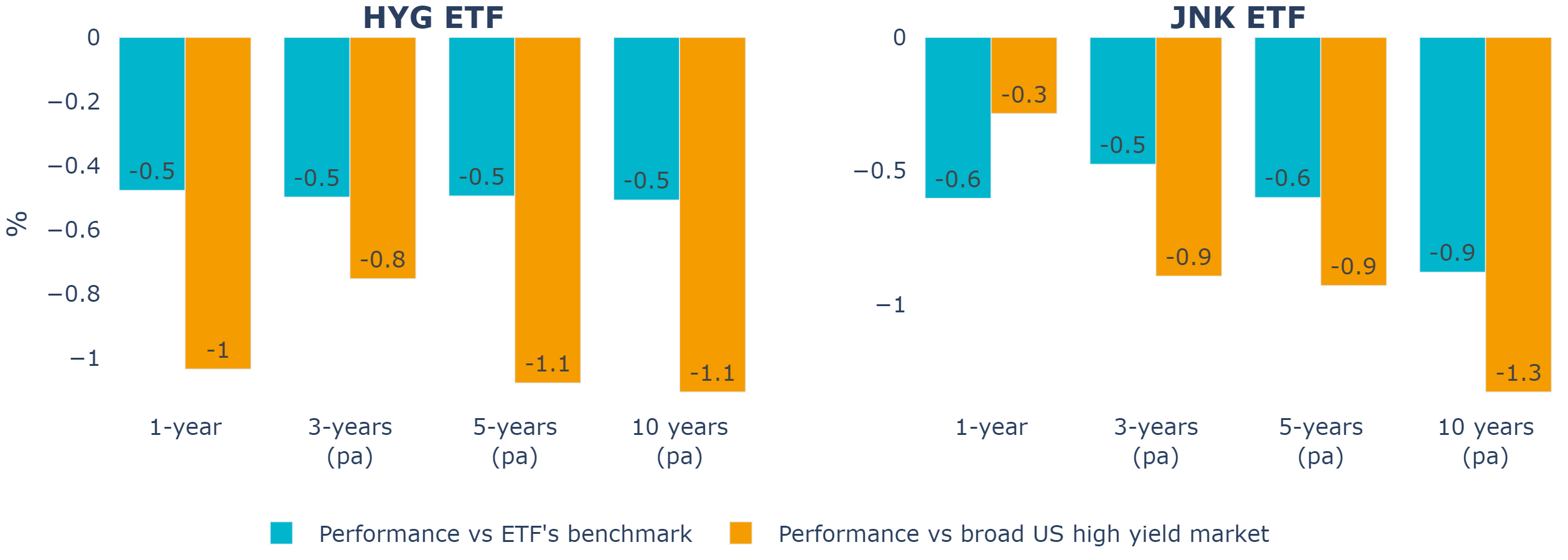

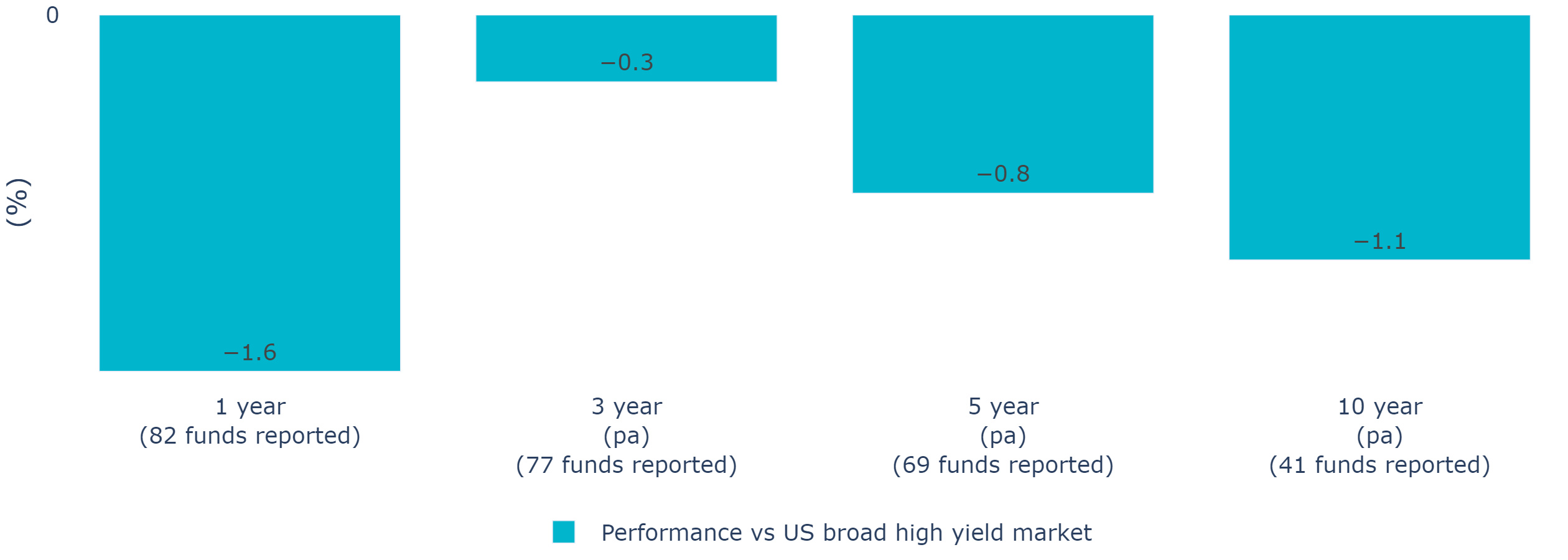

The most commonly used US high yield ETFs (with over $25bn in consolidated net assets2), the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) and the SPDR Bloomberg High Yield Bond ETF (JNK), have consistently underperformed their benchmarks and the broad US market (Figure 2).

Figure 2: US High yield ETF investors have experienced persistent underperformance1

Our analysis also shows that the median UCITS fund (passive and active) has also underperformed on a net of fee basis versus the Bloomberg US high yield corporate index (Figure 3).

Figure 3: In Europe, the median UCITS high yield fund has also underperformed the broad index3

Liquidity is a major hurdle

Poor liquidity, wide bid/ask costs and costly manager fees in US high yield (a consequence of post-2008 era banking regulations) have been major factors for this widespread underperformance. The ETFs in Figure 2 even track “liquid” US high yield indices and as a result sacrifice illiquidity premia from the smallest, least accessible issuers.

Additionally, fundamental active managers typically suffer concentration risks due to resource cons traints. They often rely on credit analysts to deliver alpha, but even the most well-resourced team could never attempt to fully cover the 900 unique issuers in the US

high yield index. The result is relatively concentrated active portfolios. We find 50% of fundamental active US high yield managers hold fewer than ~300 bonds (less than ~15% of the index)3.

But there is a solution!

We believe ‘credit portfolio trading’ is a solution to the liquidity problem. We pioneered this trading protocol in 2012 by exploiting liquidity within the ETF ecosystem. We find can reduce US high yield transaction costs from 60bp-80bp (for traditional over-the-counter trading) to 10bp-20bp, even for thinly-traded bonds (essentially earning a free illiquidity premium).

This involves trading ‘baskets’ of bonds. We find we can transact $500m of bonds in a single day, cutting execution times to hours, rather than days or weeks. In our view this is essential when dealing with fleeting value in hard-to-access bonds.

Reducing trading costs can go a long way to matching the benchmark, but fully meeting it requires enough alpha to offset remaining trading costs. We believe a systematic approach can consistently achieve this.

How does a systematic fixed income approach work?

Systematic approaches make use of structured data, quant research and computing power for alpha positioning.

Our proprietary models aim to identify fundamental value and mispricing opportunities, allowing us to tilt portfolios towards the most attractively priced bonds, and away from bonds where expected returns do not justify the risks. A well-calibrated model can analyse a whole bond universe, quickly and repeatedly. This is a huge advantage in a market with thousands of bonds – where a traditional active manager is limited by credit analyst coverage and research time.

As such, we can build portfolios with numerous active “micro positions”, rather than the large, concentrated positions common in most traditional fundamental active strategies. We also target often-fleeting alpha opportunities in less liquid bonds.

A systematic strategy is likely to create a uniquely-structured portfolio. Our strategy, for example, has an alpha correlation of less than 0.25 with 90% of the fundamental active US high yield manager universe, and a negative correlation with 60% of it.

Systematic approaches are innovative, but not new

Key to our approach is integrating portfolio management, research, and trading disciplines within a single team to challenge conventional thinking. This helped us develop our proprietary trading protocols and our systematic approach.

Our US high yield strategy has a decade-plus track record of aiming to match the broad US high yield index net of costs and charges.

We believe now is the time for investors to optimize their US high yield allocations. A systematic approach could be the answer.