Australia

Australia

01 November 2024

Multi-asset

Week to 08 November 2024

Chart of the week

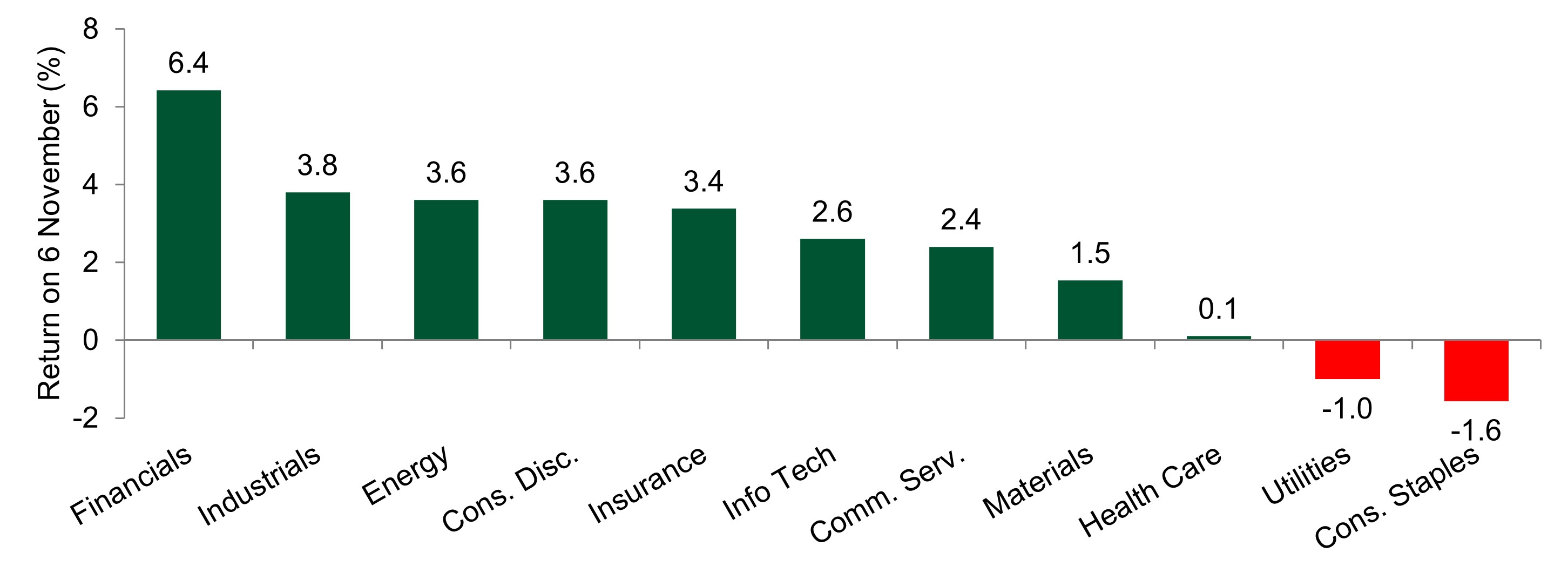

Financials were the top performing US sector after Trump’s Victory

Source: Insight Investment and Bloomberg as at 8 November 2024.

- Financials were the top performing US sector following Donald Trump’s victory in the US election this week. This was mainly driven by the banks (+11.7%) which are expected to benefit from potential deregulation and a stronger growth backdrop. The relative losers were those areas of the markets more sensitive to interest rates, such as utilities and consumer staples, who struggled in the face of a 16 basis point rise in 10-year US Treasury yields.

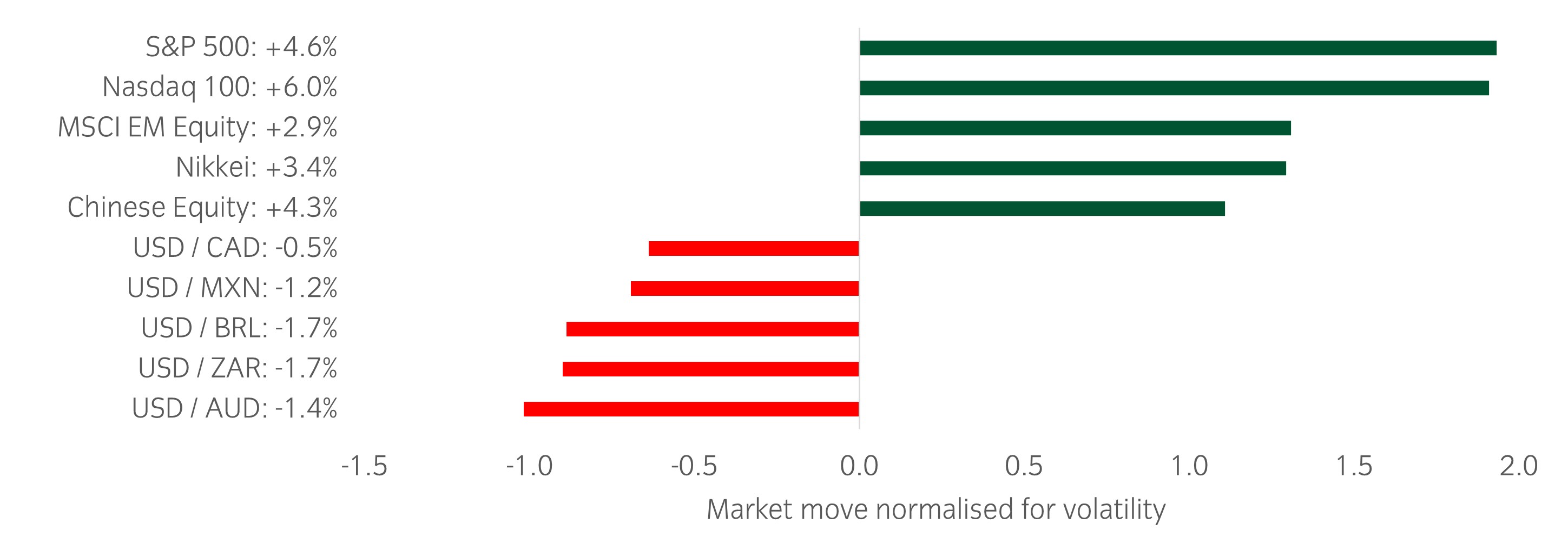

Significant market moves this week

Source: Bloomberg and Insight as at 8 November 2024. The price movement of each asset is shown next to its name. The data used by the bar chart divides the price movement by the annualised historical volatility of each asset.

Winners & losers: US equities posted strong returns on the week alongside the Nikkei, which gained off the back of a weaker yen. The dollar weakened against cyclical currencies such as the Australian Dollar and South African Rand.

Over the past week, several things caught our eye:

- A busy week was dominated by the US election, in which Donald Trump secured the presidency and the Republican Party looks to have secured control of the House and Senate. Initial market moves were positive for US equities and the US dollar, while Treasury yields jumped higher as Trump’s policy agenda looks to be more inflationary than that of Harris.

- Major central banks continued to cut rates with both the Federal Reserve and Bank of England cutting interest rates by 25bp, as widely expected. Fed Chair Jerome Powell decided to avoid discussing the potential impact of the US election, saying “We don’t know what the timing and substance of any policy changes will be”. It has been reported that Trump will allow Powell to serve out his term as Fed Chair which is due to end in May 2026.

- The main economic data released this week was the US ISM Services Index and it was much stronger than expected. October’s level of 56 comfortably exceeded the consensus of 53.8 and is the strongest number in over 2 years. Manufacturing remains in a slump but improving forward indicators, alongside strong services data, are enough to allay growth concerns.

Asset allocation observation

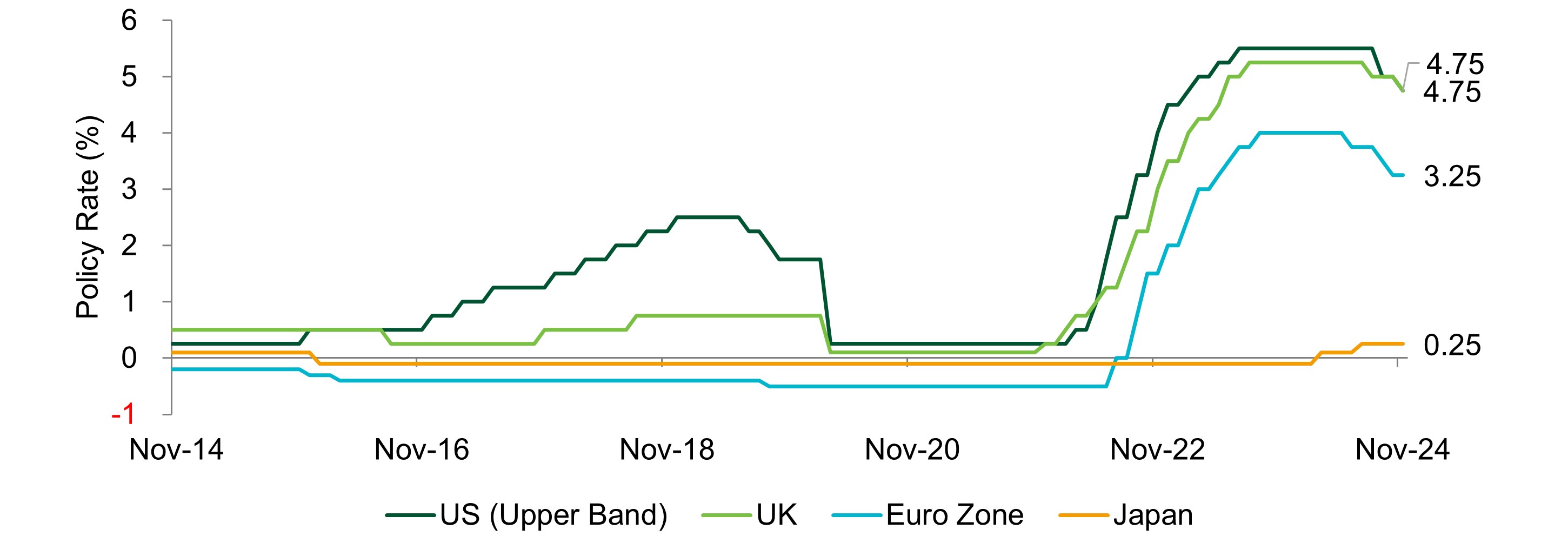

Central banks are in easing mode (ex Japan)

Source: Insight and Bloomberg as at 8 November 2024.

- The global easing cycle continued this week with the Bank of England and Federal Reserve lowering their rates to 4.75%. While Japan remains a relative outlier, with more hikes expected over the next year, the combination of easing financial conditions and fiscal impulse in the US is constructive for risk assets.

- The portfolios have been adding upside exposure to equities, looking to capitalise from a US led rally into year end.

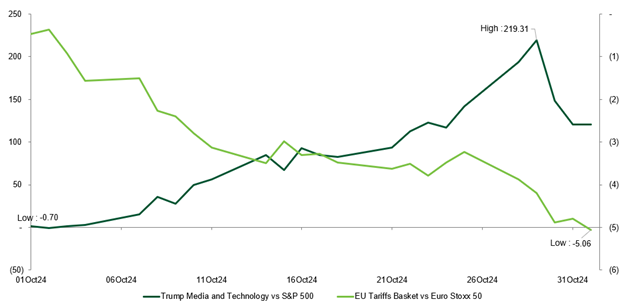

Week to 01 November 2024

Chart of the week

Trump media's surge against US equity and EU tariff woes against European equities

Source: Insight Investment, Barclays and Bloomberg as at 1 November 2024.

- As we race towards the US elections, markets are likely to experience increased volatility driven by the expected divergent policies of either a Trump or Harris victory. Whilst it is still a close call over who will win, over recent weeks we have seen a shift in market sentiment, partly reflected in the contrasting performance of assets. For example, Trump Media’s outperformance relative to the broader S&P 500 has seen gains, whereas stocks that could be most negatively impacted by tariffs and any trade war have struggled.

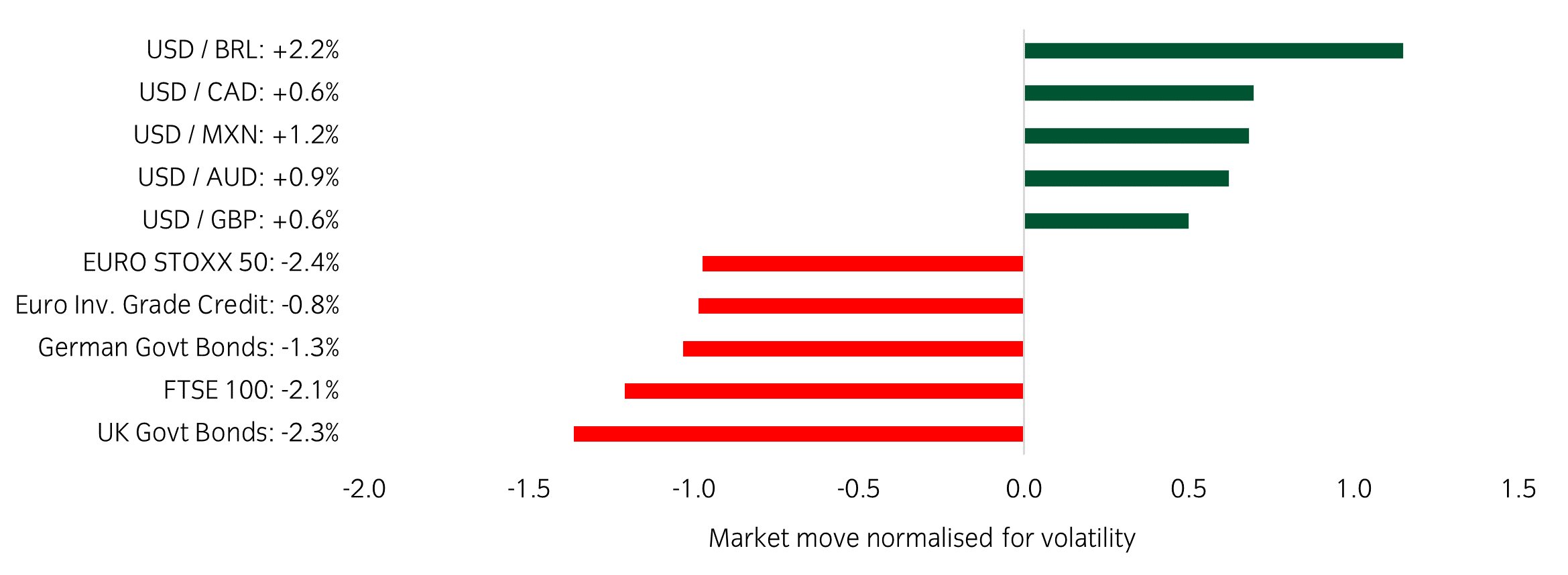

Significant market moves this week

Source: Bloomberg and Insight as at 1 November 2024. The price movement of each asset is shown next to its name. The data used by the bar chart divides the price movement by the annualised historical volatility of each asset.

Winners & losers: The US dollar continued its strong run this week, while UK equity and government bonds have suffered after the Autumn Budget announcement.

Over the past week, several things caught our eye:

- As of today, 73.5% of the S&P 500's market cap has reported, including six of the 'Magnificent 7' companies. For these six companies, price reaction to the results announcements was mixed. Tesla, Alphabet and Amazon saw a positive reaction, while reaction to the results from Microsoft, Apple and Meta was negative.

- On Wednesday, UK’s Labour government announced its Autumn Budget with measures to bridge a £22 billion fiscal gap. It aims to raise approximately £40 billion from tax increases while easing borrowing limits to fund growth-oriented investment. Gilts and the FTSE 100 Index struggled immediately after, although a recovery is partially underway on Friday.

- Ahead of the Fed’s decision next week, the US jobs report was weaker than expected, although the data is challenging as a result of Hurricane Milton’s impact.

Asset allocation observation

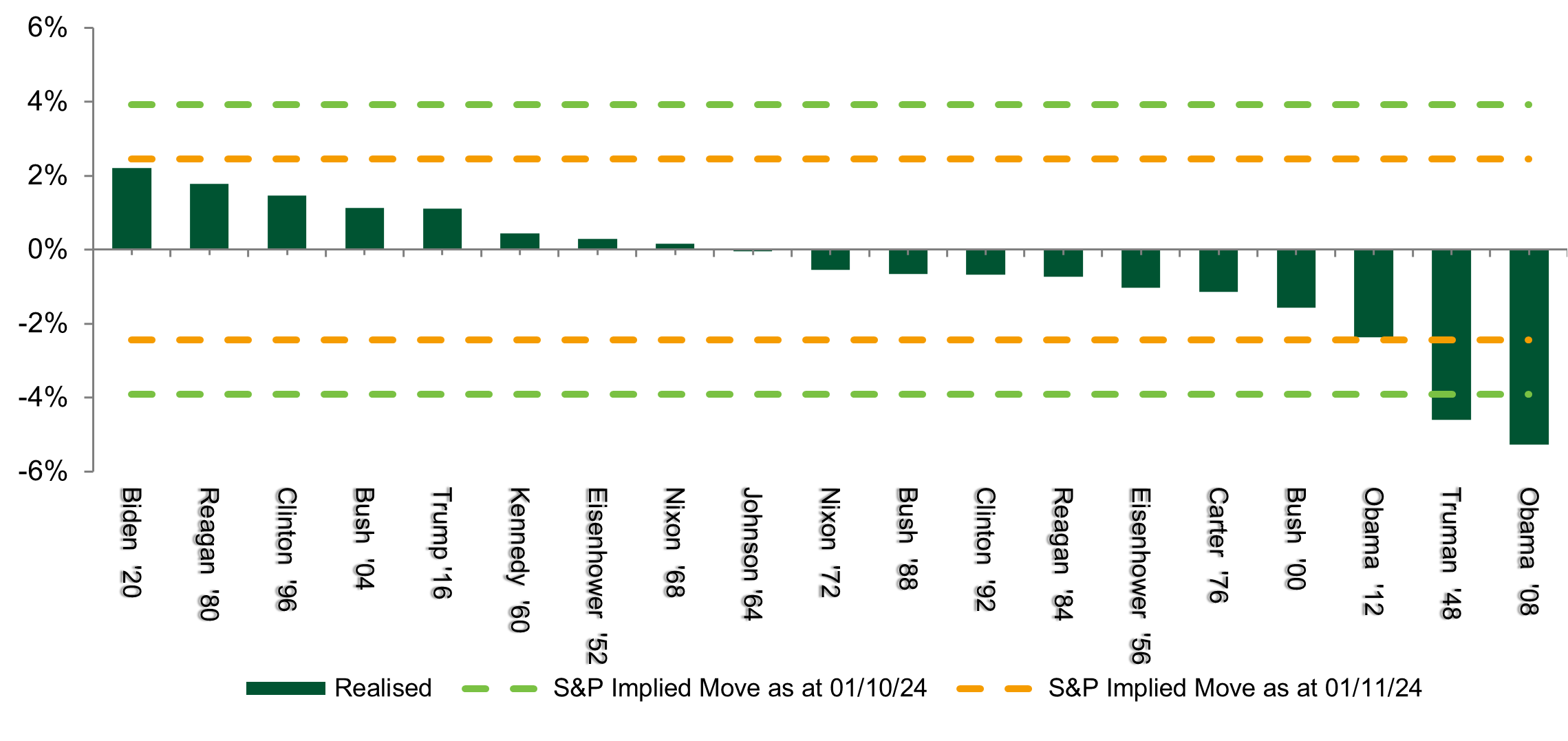

SPX implied move